For an early-stage startup looking to raise capital, wading through and making sense of all the different types of equity raises to be had can quickly become overwhelming. They’re all different, and what works for a large, growing company may not be best for an early-stage startup, so we’re walking through the equity alphabet from A to D.

What are the Differences Between Regulation A, Regulation Crowdfunding, and Regulation D?

The main differences between the three lie in:

- How much companies can raise under each

- Who they can solicit their offering to

- Who is eligible to invest in their offering

- How much the offering costs

- The amount of regulatory oversight

Regulation A

Regulation A was amended under Section 402 of the JOBS Act, resulting in a two-tiered Regulation A+. Raising under Reg A is open to US and Canadian issuers, general solicitation of the offering is permitted, and there are no restrictions on the subsequent resale of the securities offered. It’s sort of like a mini-IPO without going public.

Under Tier I, a company can raise up to $20 million in a 12-month period from accredited and nonaccredited investors. Tier 2 increases that amount to $50 million and nonaccredited investors are subject to certain investment limitations.

Both Tier 1 and Tier 2 mandate certain filings with the SEC, namely the offering materials, two years of financial statements, and an exit report. Offerings made under Tier 2 are subject to slightly more stringent reporting requirements. They must make certain state filings, the financial statements submitted to the SEC must be audited, and they must make ongoing annual and semi-annual reports after the offering is closed.

A company can only accept payment for the sale of securities offered under Regulation A after SEC staff have reviewed and qualified its offering materials. Tier 1 offerings are additionally subject to state review and qualification in any states in which the securities are to be offered for sale.

Conducting a raise via Regulation A is significantly less expensive than an IPO, but issuers should be prepared to pay significant legal fees and plan with an eye towards the several weeks it can take to receive qualification of an offering statement.

As a result, many early-stage companies opt to raise funds via the more traditional Regulation D route instead.

Who Is Regulation A Best For?

Due to the high costs involved, Regulation A is often better suited to more mature companies who have a large, active audience and who are seeking capital to fuel growth.

Regulation Crowdfunding

Regulation Crowdfunding (or CF), also known as equity crowdfunding or Title III crowdfunding, was adopted under Title III of the JOBS Act in 2016. Under it, US companies may raise up to $1.07 million in a from both accredited and non-accredited investors, and general solicitation of the offering is permitted with some limitations. Additionally, Regulation Crowdfunding offerings must be offered through an online platform operated by an intermediary registered either as a broker-dealer (such as MicroVentures) or a registered funding portal.

Who Is Regulation Crowdfunding Best For?

Companies who tend to successfully raise through Regulation Crowdfunding are typically between the Seed to Series A funding stage and have a minimum viable product (MVP), plus early customer feedback. Companies who have a large base of passionate fans are even better suited for this type of raise.

Is Equity Crowdfunding Right for Your Startup?

Regulation D

Unlike a Regulation A raise, accredited investors and a very limited number on nonaccredited investors can participate in a Regulation D raise. As a quick refresher, as determined by the SEC, accredited investors are entitled to access such investment opportunities if they satisfy at least one requirement regarding their income, net worth, assets, governance status, or professional experience.

Because Regulation D offerings are generally only available to accredited investors, they are exempt from certain registration and other requirements for a company selling equity. Under Regulation D there are two options:

- 506(b)

- 506(c)

Under 506(b), companies may not generally solicit investors; i.e., they cannot publicly announce or advertise that they are fundraising to potential investors they don’t already know (unless there is a broker/dealer involved to introduce them). Under 506(c), companies are allowed to generally solicit; however, there is the additional burden of obtaining documented verification that all investors meet the accredited investor criteria.

Whether a company is looking to raise a (relatively) small amount from a few investors or a large amount of money from venture capitalists and institutional investors, Regulation D can be highly appealing to companies because there are no limits on how much they can raise and they are not required to complete the extensive filings required of companies raising under Regulation A. Instead, they must make a Form D filing within 15 days of the first sale of securities in the offering and additionally make certain state “notice filings” when their securities have been purchased by a resident of that state.

Who Is Regulation D Best For?

Offerings under Regulation D are typically best suited for early-stage startups that are at Seed or Series A rounds of funding and who have begun generating significant revenue and substantial top-line and/or user growth.

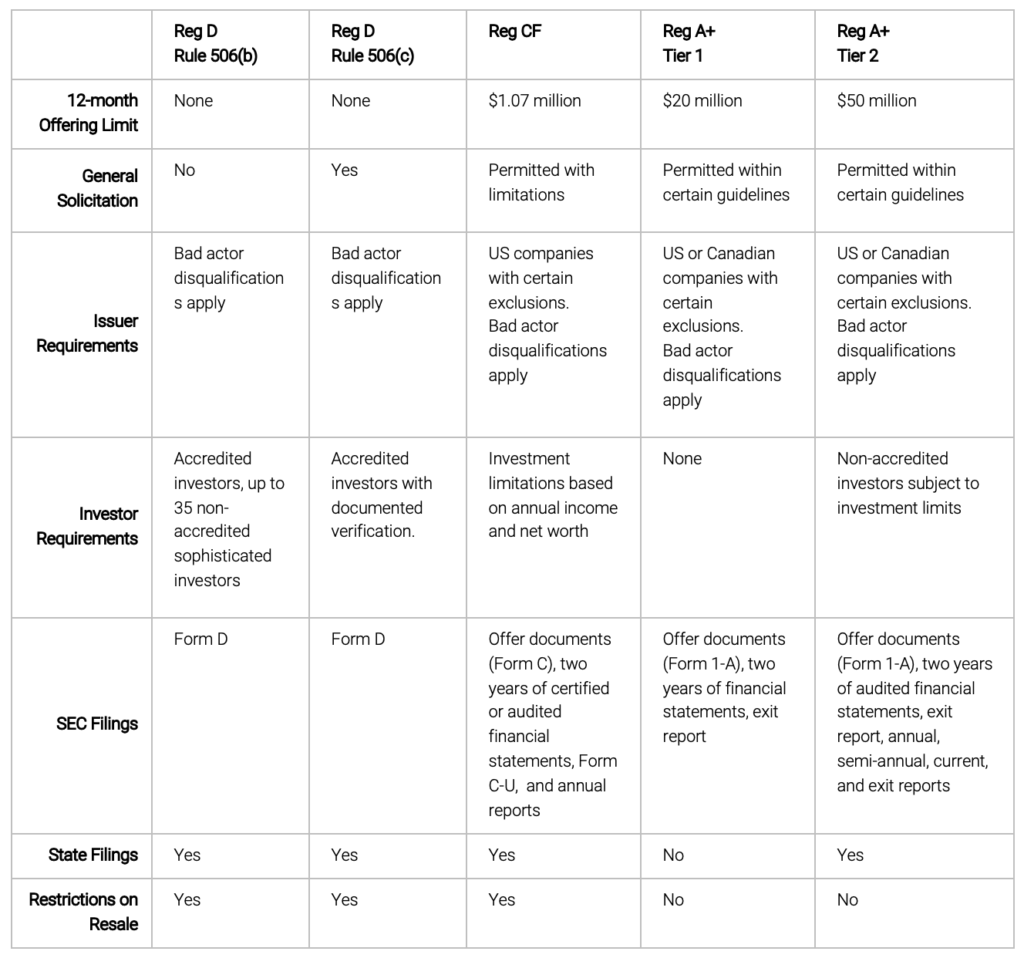

The following is a very high-level comparison of the offering types discussed here:

Currently, MicroVentures has the capability to conduct raises for startups through Regulation D 506, Regulation A, and Regulation Crowdfunding. If you’re interested in raising money for your startup, you can apply for an offering. If you’re not sure what type of offering is best for you, we’re happy to discuss which option may be best suited for your business.

*****

The information presented here is for general informational purposes only and is not intended to be, nor should it be construed or used as, comprehensive offering documentation for any security, investment, tax or legal advice, a recommendation, or an offer to sell, or a solicitation of an offer to buy, an interest, directly or indirectly, in any company. Investing in both early-stage and later-stage companies carries a high degree of risk. A loss of an investor’s entire investment is possible, and no profit may be realized. Investors should be aware that these types of investments are illiquid and should anticipate holding until an exit occurs